Just Keep Buying Book Summary (Part 2): Investing Lessons to Grow Your Wealth

In the first part of Just Keep Buying by Nick Maggiulli, we explored how smart saving habits build a strong financial base – from understanding how much to save, when to spend, and why consistency matters more than perfection. Now, in this second part of the Just Keep Buying Book Summary, we move beyond saving into the world of investing. Here, Nick Maggiulli reveals practical lessons on when to invest, how to handle market volatility, and why staying invested beats market timing. If the first part was about building your foundation, this part is all about growing your wealth and making money work for you – steadily and intelligently.

Chapter 11: Smart Investment Choices for Long-Term Growth

Everyone’s Path to Wealth Is Different

In Just Keep Buying, Nick Maggiulli emphasizes that there’s no single formula for building wealth – what works for one person might not work for another. The key is to consistently invest in income-generating assets that fit your personal goals and risk tolerance.

While many financial experts talk only about stocks and bonds, Nick expands the conversation by introducing other options – including real estate, farmland, small businesses, and even digital products. Each investment type carries its own advantages and challenges, and understanding them helps you build a strong, diversified portfolio.

1. Stocks – The Long-Term Wealth Builder

Stocks represent ownership in a company and have historically delivered some of the highest returns. According to Nick Maggiulli’s research, U.S. stocks have averaged about 7% annual returns over the past 200 years – outperforming most other markets.

However, the stock market is volatile. You might see a 50% drop once a century, 30% every few years, and 10% corrections almost every other year. But as Nick reminds readers in Just Keep Buying, time is the best friend of an equity investor.

To manage risk, diversify your holdings using index funds, ETFs, or a mix of individual stocks. The longer you stay invested, the smoother the returns become.

2. Bonds – Stability in a Volatile World

After stocks, bonds are another key component of a balanced portfolio. Bonds are essentially loans you give to governments or corporations in exchange for regular interest payments.

Nick Maggiulli recommends U.S. Treasury Bonds for their reliability and low risk. Bonds come in different maturity types:

- Treasury Bills: 1–12 months

- Treasury Notes: 2–10 years

- Treasury Bonds: 10–30 years

Why Invest in Bonds:

- They usually rise when stocks fall, providing stability.

- They offer a steady income stream through interest.

- They provide liquidity for emergencies or portfolio rebalancing.

- Real Estate – Building Wealth You Can See

3. Real Estate – Building Wealth You Can See

Investing in property is one of the most popular ways to generate passive income. You can either live in your property or rent it out to earn returns that typically range between 12% and 15% annually.

You can invest directly by buying properties or work with real estate agents to find good deals. Negotiating directly with sellers can also help you get a better price.

4. REITs – Real Estate Without the Hassle

If you want exposure to real estate without managing tenants or maintenance, REITs (Real Estate Investment Trusts) are a great option. A REIT is a company that owns and manages income-producing properties like apartments, offices, or warehouses.

They’re available as:

- Publicly traded REITs – bought like stocks

- Private REITs – limited access but higher potential returns

- Public non-traded REITs – a mix of both worlds

REITs allow you to benefit from real estate returns while staying completely hands-off.

5. Farmland – The Inflation Hedge

Farmland is another stable investment that rarely loses value. It offers annual returns of 7–9% and has a low correlation with stocks and bonds, meaning it performs differently when markets fluctuate. Plus, farmland provides a natural hedge against inflation, since food demand never goes away.

6. Small Businesses and Angel Investing

Nick Maggiulli explains that investing in small businesses or franchises can lead to massive returns – but it depends on your role.

If you’re an owner-operator, you’ll need to put in long hours and manage day-to-day operations. However, if you’re an owner only, you can enjoy passive income without the stress of daily management.

Similarly, angel investing – funding early-stage startups – can yield 20–25% annual returns but comes with high risk. Diversifying across multiple startups increases your chance of hitting a big win.

7. Royalties – Earning from Creativity

Royalties are payments for using intellectual property such as music, films, books, or trademarks. Platforms now allow investors to buy and sell royalty rights, creating income from someone else’s creative work.

For example, owning the rights to a popular song or digital asset could earn you recurring revenue every time it’s used or streamed.

8. Your Own Products – The Most Powerful Asset

Finally, Nick Maggiulli reminds readers that one of the best investments you can ever make is in your own products. These could be digital creations like eBooks, software, or AI tools – or physical products with long-term demand.

Unlike traditional investments, your own products don’t rely on market fluctuations – they rely on your creativity and effort. A digital course or website, for instance, can continue generating income for years with minimal upkeep.

Just Keep Buying Key Takeaways from Chapter 11

- There’s no universal formula for investing – personalize your portfolio.

- Stocks build long-term wealth but require patience and consistency.

- Bonds provide safety and balance during market volatility.

- Real estate and REITs offer steady passive income opportunities.

- Farmland and small businesses diversify and strengthen your portfolio.

- Investing in your own products can create unlimited earning potential.

- As Nick Maggiulli explains in the Just Keep Buying Book, the ultimate goal is to keep buying income-producing assets – because time and consistency are the real wealth builders.

Chapter 12: The Truth About Picking Individual Stocks

The Emotional Rollercoaster of Stock Picking

In Just Keep Buying, Nick Maggiulli shares a story about one of his friends who decided to invest in individual stocks. Within hours of buying, the stock price fell, leaving his friend stressed, anxious, and filled with regret. This experience shows how emotional investing can be when you rely on single-stock bets rather than diversified strategies.

When you buy individual stocks, your emotions often take over. A single bad trade can cause sleepless nights and panic decisions – proof that mental peace matters as much as returns in investing.

The Financial Reality: Most Stock Pickers Lose

Nick Maggiulli highlights the SPIVA Report, which evaluates the performance of fund managers worldwide. Over a five-year period, about 75% of funds fail to beat their benchmark index. That means even professional investors with years of experience and advanced tools struggle to outperform simple index funds.

To make it even clearer, consider this: out of the 20 companies listed in the Dow Jones Industrial Average in 1920, none remained in the index a hundred years later. Businesses change, industries evolve, and even market leaders eventually fade. That’s why, as Nick says in the Just Keep Buying Book, buying index funds or ETFs is a smarter long-term strategy than trying to find “the next big winner.”

The Skill Myth: Are You Really Good at Picking Stocks?

Nick Maggiulli raises an honest question – how do you even know if you’re good at stock picking?

The results of individual stock decisions take years to reveal themselves. By the time you know whether your choice was good or bad, the market has already moved on. Research shows that only about 10% of professional stock pickers consistently perform better than the market over time – meaning 90% of people don’t have sustainable skill in picking winning stocks.

So if full-time experts can’t do it, the odds for regular investors are even lower.

The Better Alternative: Let the Market Work for You

Instead of chasing short-term stock gains, Nick recommends focusing on broad-based investments like index funds or ETFs. These allow you to own hundreds (or even thousands) of companies at once – reducing risk and emotional stress.

If you still enjoy picking individual stocks, treat it like a hobby, not a wealth strategy. Track your returns carefully – monthly or yearly – and compare them with an index fund. Most people eventually realize that consistent investing beats constant guessing.

For example, if you invest $10,000 in an index fund tracking the S&P 500, you’re instantly diversified across top U.S. companies. But if you put the same $10,000 into one company, your outcome depends entirely on its success or failure – a much riskier bet.

Just Keep Buying Key Takeaways from Chapter 12

- Individual stock picking causes emotional and financial stress.

- According to Nick Maggiulli, over 75% of funds fail to beat the market.

- Even professional investors rarely outperform index funds consistently.

- The Just Keep Buying Book emphasizes that diversification wins over speculation.

- If you still want to pick individual stocks, treat it as fun – not as a strategy for serious wealth building.

- Index funds and ETFs offer simplicity, diversification, and peace of mind – the real pillars of long-term investing success.

Chapter 13: The Best Time to Start Investing

Time Waits for No Investor

In Just Keep Buying, Nick Maggiulli highlights one simple truth – the longer you wait to invest, the more you lose. History has shown that even during the darkest times – world wars, economic recessions, or pandemics – the market has never stopped moving forward.

Warren Buffett often says, “The best time to start was yesterday. The next best time is today.” The idea is simple: markets grow with time, and the sooner your money enters, the sooner it starts compounding.

Imagine a girl named Siya, who receives $1 million as a gift from her mother. She has two choices:

- Invest the full amount right now, or

- Invest 1% each year for the next 50 years.

If Siya invests all her money today, it will start compounding immediately. But if she delays and invests slowly, her money loses value to inflation and she ends up buying at higher prices over time. As Robert T. Kiyosaki says, “Don’t work for money, let your money work for you.”

Lump-Sum vs. Investing Over Time

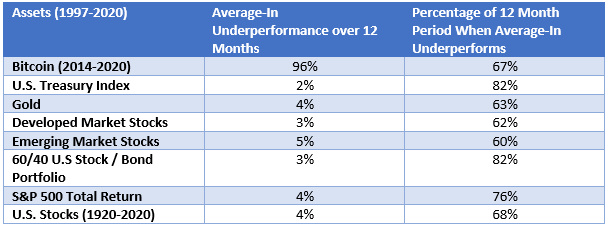

Nick Maggiulli, in the Just Keep Buying Book, compares two strategies:

- Buy Now (Lump-Sum Investing): Putting all your available money into the market at once.

- Average-In (Dollar-Cost Averaging): Spreading your investments gradually over time.

So, which one performs better?

According to long-term studies, Average-In underperforms Buy Now by about 4% in most 12-month rolling periods between 1997 and 2020.

However, Average-In tends to perform better only when the market crashes – which doesn’t happen every year. Since big crashes occur once in a decade or two, waiting for the “perfect time” to invest often costs more than it saves.

Performance Comparison (1997–2020)

As the data shows, Buy Now wins the majority of the time – proving that staying invested is more powerful than timing your entry.

Understanding the Risk Factor

Of course, investing all your money at once feels riskier – and that’s true to some extent. Lump-sum investing has a higher short-term volatility (standard deviation), meaning your portfolio may fluctuate more.

But risk can be managed through diversification. A 60/40 portfolio (60% stocks and 40% bonds) offers a balanced approach – reducing volatility without sacrificing long-term growth.

Interestingly, when comparing Average-In with the S&P 500 versus Buy Now with a 60/40 portfolio, the lump-sum 60/40 strategy still outperformed on average. This means that even a balanced, diversified approach works better than waiting too long to invest.

Just Keep Buying Key Takeaways from Chapter 13

- Time in the market beats timing the market. The earlier you invest, the more your money compounds.

- Nick Maggiulli emphasizes that history rewards those who act, not those who wait.

- Lump-sum investing generally outperforms average-in investing about 75% of the time.

- Waiting for a market crash rarely pays off because major dips are unpredictable.

- Diversify your portfolio – a 60/40 stock-bond mix can reduce risk while keeping you invested.

- As Just Keep Buying reminds us – the market, like time, waits for no one. Start today, and let compounding do the heavy lifting.

Chapter 14: Don’t Wait for the Perfect Market Moment

The Myth of “Buying the Dip”

In the Just Keep Buying Book, Nick Maggiulli challenges one of the most common beliefs in investing – the idea that you should “buy the dip.”

On paper, it sounds brilliant: save money, wait until the market crashes, and then invest at a discount. But in reality, this approach rarely works. Why? Because predicting a market dip is like trying to predict when it will rain three months from now – even experts can’t do it consistently.

Understanding DCA vs. Buy the Dip

To explain this concept clearly, Nick Maggiulli compares two investment strategies:

- Dollar Cost Averaging (DCA) – You invest $100 every month for 40 years, no matter what the market does.

- Buy the Dip – You save $100 each month but only invest when the market falls significantly.

Now, imagine someone who has a “magical power” to detect every dip perfectly – even then, the results are surprising. When Nick tested this using U.S. stock market data from 1920 to 1980, the “Buy the Dip” strategy underperformed DCA nearly 70% of the time.

The reason is simple: severe market dips are rare. They don’t happen every year – sometimes not even every decade. Meanwhile, those who consistently invest through DCA keep benefiting from market growth and compounding returns without waiting on the sidelines.

Why Waiting Costs You More?

Let’s take a real-world example:

Suppose John, an average investor, started investing randomly each month from 1926 into a broad U.S. stock index. If he simply kept buying – without worrying about dips or crashes – history shows that:

- He would have outperformed cash holdings 98% of the time, and

- Beaten U.S. 5-year Treasury Notes 83% of the time.

That’s the power of Just Keep Buying – staying consistent no matter the headlines or temporary market drops.

As Nick explains, saving cash to buy a dip is like keeping your car parked waiting for a green signal that never comes. You might feel safe, but you’re not moving forward.

The Core Lesson from Just Keep Buying

The purpose of this chapter is to drive home a single principle – don’t wait for the perfect time to invest. The longer your money sits idle, the more opportunities you lose to compounding and growth.

Nick Maggiulli connects this with his earlier chapters:

- Invest all at once if you can (Chapter 13)

- Don’t try to time the market (Chapter 14)

When you combine both, the message becomes crystal clear –

“You should invest as soon and as often as you can.”

Just Keep Buying Key Takeaways from Chapter 14

- “Buy the Dip” is a myth. Even perfectly timed dips underperform steady investing.

- Dollar Cost Averaging (DCA) consistently beats timing-based strategies across decades.

- Market crashes are rare, but growth happens more often – don’t sit out waiting.

- Just Keep Buying – because time, not timing, is the true friend of every investor.

- Consistency in investing creates wealth, not perfection in timing.

Chapter 15: When Luck Shapes Your Financial Future

The Hidden Force Behind Every Success

In the Just Keep Buying Book, Nick Maggiulli opens this chapter with a surprising truth – luck quietly influences almost everything, from bestselling authors to legendary investors.

Back in the 1970s, the publishing industry believed writers shouldn’t release more than one book a year. Yet Stephen King and J. K. Rowling tested this rule by publishing extra books under pen names. Initially, those titles barely sold. But once readers discovered the authors’ true identities, those same books crossed millions of sales. What changed? Not the words, not the quality – just luck and timing.

In investing, this invisible factor plays a similar role. The same mysterious force that can make a career flourish can also decide whether your portfolio grows or struggles.

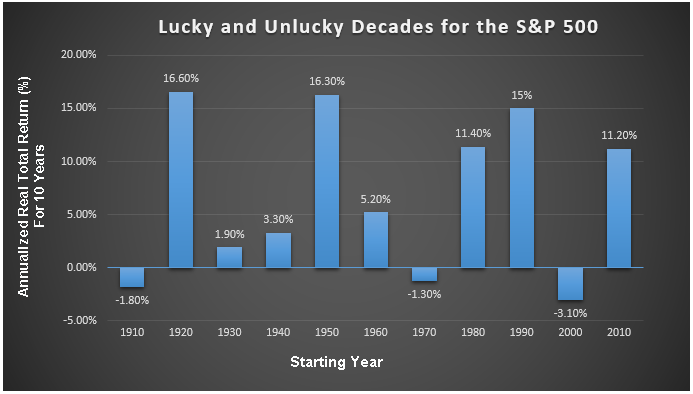

The Decade You’re Born Into Matters

Nick Maggiulli illustrates this using historical S&P 500 data from 1910 to 2010, showing how some decades were “lucky” while others were not.

Imagine two investors:

- Investor A earns 5% more than the market each year.

- Investor B earns 5% less than the market each year.

If Investor B starts during a booming decade while Investor A begins just before a market crash, the “unlucky” timing can easily reverse their outcomes. In short, when you invest often matters more than how smart you invest.

Why the Order of Returns Changes Everything?

Let’s say you earn +15% and +10% in your first two years, then face –10% and –15% in the next two.

If you invest a lump sum and never add money, your final result will roughly balance out.

But in real life, most people add new money regularly – every month or every year. That means your future returns carry more weight because more money is invested later.

If those later years are bad, your total portfolio suffers more.

Here’s a simple example:

Imagine investing $5,000 per year.

If market losses happen early, you might still recover over time.

But if big losses hit after 20 years of growth, you could lose over $100,000 more compared with an early downturn.

This shows why sequence of returns risk – the order in which gains and losses happen – can make or break your financial future.

How to Protect Yourself from Bad Luck?

You can’t control luck, but you can build a portfolio that minimizes its damage.

Nick Maggiulli suggests three practical steps, especially for those nearing retirement or relying on investment income:

- Diversify with lower-risk assets such as bonds or gold.

These act as stabilizers when markets crash. - Withdraw less during downturns.

Reducing withdrawals gives your portfolio time to recover. - Stay flexible with income.

Consider part-time work or a side project to ease pressure on your savings.

As Nick notes, a bad year won’t ruin your future – a bad decade might. Diversification and patience are your best defenses against unlucky timing.

The Core Message of Just Keep Buying

Luck plays a role in every investor’s story, but consistency beats prediction. You can’t forecast when markets will shine, but you can control how often you show up and invest.

Even the world’s best investors can’t escape the randomness of markets – but by continuing to “Just Keep Buying”, you shift the odds in your favor over the long run.

Just Keep Buying Key Takeaways from Chapter 15

- Luck matters – both in careers and in investing. Timing can shape your results as much as skill.

- Sequence of returns affects long-term growth; losses later in life hurt more than early ones.

- Diversification and flexibility help protect against unlucky decades.

- Don’t fear randomness – embrace consistency. Keep investing, keep building.

- The most successful investors aren’t the luckiest – they’re the ones who keep showing up.

Chapter 16: Embracing Market Storms – Don’t Fear Volatility

Taking Risks Is Sometimes the Safest Move

In the Just Keep Buying Book, Nick Maggiulli begins this chapter with an unforgettable story.

When Fred Smith, founder of FedEx, had only $5,000 left in the company account and needed $27,000 to keep it alive, he took a desperate gamble – he flew to Las Vegas, played blackjack, and won enough to cover the bills. That single bold move saved FedEx.

The lesson?

Sometimes, the biggest risk is taking no risk at all.

In investing, avoiding volatility might feel safe – but it can quietly destroy your long-term wealth.

The Price of Admission to Wealth

Every reward in the financial world comes with a ticket cost – volatility.

To build wealth, you must be willing to ride through temporary declines. But how much should you tolerate?

Imagine you own a magical book that perfectly predicts the stock market. It tells you that in 2026, markets will fall by 40 percent. Would you stay invested or move to bonds?

Nick Maggiulli explains that if you avoid every 5 percent dip and move all your money into bonds, your wealth could end up 90 percent smaller than if you had simply stayed invested in stocks. That’s because every time you flee the market, you miss the rebound – and missing those rebounds costs far more than temporary losses.

Data shows that if you invest in bonds only when markets fall 15 percent or more and stay in stocks the rest of the time, you can still build long-term wealth. But raising that threshold further makes results worse – because bigger dips usually follow bad years.

Volatility isn’t your enemy – exiting too often is.

You Don’t Need a Magic Book – You Need Diversification

There’s no perfect guide that tells you when markets will crash or recover.

What we have instead is diversification – the power to spread risk across different assets like stocks, bonds, real estate, or index funds.

Buying a diverse set of income-producing assets over time, instead of all at once, helps smooth out the bumps of volatility. You won’t eliminate market swings, but you can make sure no single dip wipes out your financial future.

As Nick Maggiulli reminds us throughout Just Keep Buying, volatility isn’t a bug – it’s the price of admission for building lasting wealth.

A Simple Way to Think About Volatility

Picture a roller coaster. If you jump off midway because it drops too fast, you’ll never experience the climb that follows. Markets behave the same way – every dip, crash, and panic eventually gives way to recovery.

So instead of waiting for the “perfect” moment, keep buying through every market condition. The ups and downs are just noise – the direction over decades is up.

Just Keep Buying Key Takeaways from Chapter 16

- Volatility is the cost of growth. You can’t earn higher returns without accepting short-term swings.

- Avoiding drawdowns hurts more than it helps. Constantly moving into bonds after small dips drastically reduces long-term wealth.

- Diversify smartly. Hold a mix of income-producing assets – stocks, bonds, and real estate – to smooth out volatility.

- Stay invested. Even when markets feel scary, history proves recovery rewards those who don’t exit early.

- The golden rule: Don’t wait for calm seas – build your ship strong enough to sail through storms.

Chapter 17: Turning Market Crashes into Opportunities

The Hidden Wisdom in Market Panic

In Just Keep Buying, Nick Maggiulli reminds us of an old quote from 18th-century banker Baron Rothschild – “The time to buy is when there’s blood in the streets.”

This saying captures a timeless truth: the best buying opportunities often appear when fear dominates the market.

But here’s the catch – waiting endlessly for a crash to “buy low” rarely works. Most investors who hoard cash for the next dip end up missing out on years of market growth. Market crashes are rare, unpredictable, and often recover faster than anyone expects.

However, if you do find yourself with extra cash during a crash – that’s when opportunity meets courage. As Nick Maggiulli puts it in the Just Keep Buying Book, “Buying during chaos is uncomfortable, but it’s one of the few times you get paid for your bravery.”

Why Market Crashes Create Big Upside?

Let’s understand this with simple math.

When the market drops, the percentage gain required to recover is always larger than the percentage loss:

- A 10% loss needs an 11.1% gain to break even.

- A 20% loss needs a 25% gain.

- A 50% loss needs a 100% gain!

That’s why a 50% crash sets up massive potential returns once the recovery begins.

Between 1930 and 1936, investors who stayed invested saw nearly 3x growth as markets rebounded.

The idea isn’t that every crash will triple your money – but many crashes offer 50%–100% upside once fear fades and markets stabilize.

Reframing the Upside: A Smarter Way to See Losses

During the 2020 market crash, stocks fell by roughly 33%. Many investors panicked and sold – but Nick Maggiulli challenged readers to think differently: How long will it take to recover?

Here’s the math formula he uses:

Expected Annual Return = (1 + % Gain Needed to Recover) ^ (1 / Years to Recover) – 1

If the market needs a 50% gain to recover:

- In 1 year, your annual return = 50%

- In 2 years, = 22%

- In 3 years, = 14%

- In 4 years, = 11%

- In 5 years, = 8%

Even if it takes five years, an 8% annual return is still excellent – and that’s the mindset difference between fear and opportunity.

So, when markets crash, don’t ask “What if it gets worse?” Ask instead, “What will my return be when it recovers?”

The Courage to Buy When Others Run

Nick Maggiulli advises that when markets drop by 50%, that’s the time to “back up the truck” – meaning, invest as much as your financial situation allows. Historically, such moments deliver annualized returns above 25% in the following years.

But yes, there’s always uncertainty. Not every market recovers quickly – Japan’s market after 1989 is the rare example that took three decades to return to its peak. Yet, globally, such long stagnations are exceptions, not the rule.

As financial author Jeremy Siegel wisely said,

“Fear has a greater grasp on human action than the impressive weight of historical evidence.”

In other words, fear feels powerful – but history shows patience always wins.

A Real-Life Example: The Investor with Two Choices

Imagine you have ₹10 lakh to invest during a crash.

Investor A waits for the “perfect” bottom, holding cash out of fear.

Investor B starts investing gradually as prices fall.

Five years later, when the market rebounds, Investor B enjoys 70–100% gains, while Investor A still waits for “certainty.”

That’s the difference between acting on fear and acting with conviction – a core lesson from Just Keep Buying.

Just Keep Buying Key Takeaways from Chapter 17

- Crashes are opportunities, not threats. The greatest returns often follow periods of panic and fear.

- Stop waiting for the perfect dip. Market corrections are unpredictable and hoarding cash usually hurts long-term growth.

- Reframe losses. A 30–50% decline sets the stage for powerful future gains.

- Act with courage. Investing during a crash feels uncomfortable – but that’s where real wealth is built.

- History favors patience. Markets have always recovered, even after the worst downturns.

Chapter 18: The Smart Way to Sell – When and How to Exit Investments

The Hardest Part of Investing

In the Just Keep Buying Book, Nick Maggiulli explains that buying is easy – but selling is where most investors stumble. Selling tests your emotions, logic, and patience all at once.

When markets rise, you fear missing out if you sell too early. When markets fall, you fear losing even more if you don’t sell fast enough. This emotional tug-of-war makes selling one of the toughest financial decisions you’ll ever make.

Nick Maggiulli simplifies the chaos: you should sell only for three reasons –

- To rebalance your portfolio

- To exit a concentrated or losing position

- To meet a genuine financial need

If none of these apply, it’s usually best to keep holding and let your money grow. After all, selling too often can lead to tax consequences and missed compounding gains.

Buy Fast, Sell Slow – The Nick Maggiulli Rule

Nick contrasts buying and selling beautifully in Just Keep Buying:

“Buy quickly, but sell slowly.”

When it comes to investing, waiting to buy is a losing game – because the longer you delay, the more time you lose in the market.

But for selling, the rule flips. Selling over time (gradually) often works better than selling everything in one go.

Think of it like this – if you’ve built wealth over years, why dismantle it overnight? Spreading your selling over months or years helps you capture potential future gains and minimize emotional decisions.

What Rebalancing Really? Does

Throughout Just Keep Buying, Nick Maggiulli highlights that rebalancing isn’t about chasing higher returns – it’s about managing risk.

Over time, a portfolio naturally drifts from its original allocation.

For example, a 60/40 stock-bond portfolio may turn into 75/25 after years of growth in stocks. Without rebalancing, you could end up taking more risk than intended.

But here’s the catch – rebalancing by selling your high-growth assets can reduce your long-term returns and trigger taxes.

So what’s the smarter way?

The Smarter Way to Rebalance – “Just Keep Buying”

Nick Maggiulli offers a simple, elegant solution: accumulation rebalancing – or, in his words, “Just Keep Buying.”

Instead of selling your winners, use your new contributions to buy more of your underweighted assets.

Example:

Example:

Let’s say Dheeraj’s portfolio is 70% stocks and 30% bonds, but he wants to rebalance to 60/40.

Instead of selling 10% of stocks (and paying taxes), he can simply buy more bonds with his next few months’ contributions until his portfolio naturally adjusts to 60/40.

This method keeps your investments growing, avoids tax losses, and maintains a healthy risk balance – all by consistently buying.

According to data Nick shares, portfolios rebalanced through ongoing contributions experience lower drawdowns (around -35%) compared to portfolios that don’t add funds (which can dip as low as -60%).

So yes, consistency beats timing – always.

Don’t Let Emotions Decide for You

Every asset class goes through periods of underperformance. But selling just because something is temporarily “down” is often the worst move.

Remember – the market rewards patience, not panic.

If you believe in the long-term value of your investment, ride through the lows. The dips are where most future gains are born.

The True Purpose Behind Investing

In the end, investing isn’t just about numbers or beating the market.

It’s about building a life – whether that means financial freedom, spending more time with family, or fulfilling your dreams.

As Nick Maggiulli reminds us in Just Keep Buying, you invest to create a better tomorrow – not to win a short-term race.

That’s why knowing when to sell matters just as much as knowing when to buy – because your financial choices should always serve your life goals, not your fears.

Just Keep Buying Key Takeaways from Chapter 18

- Sell only for three reasons: to rebalance, reduce concentration, or meet real financial needs.

- Buy fast, sell slow. Invest quickly, but exit gradually to capture gains and minimize taxes.

- Rebalance wisely. Use accumulation rebalancing – keep buying your underweighted assets instead of selling.

- Avoid emotional selling. Don’t react to short-term dips; patience is your greatest edge.

- Invest for purpose, not panic. Selling should align with your life goals, not your fears or market noise.

Chapter 19: Smart Places to Invest – Understanding Tax & Asset Allocation

Taxes: The Hidden Partner in Every Investment

In Just Keep Buying, Nick Maggiulli explains that knowing where to invest is just as important as what to invest in. You might pick the perfect stock or fund – but if you ignore taxes, your returns can quietly shrink over time.

Taxes decide how much of your gain you actually keep, so choosing the right investment account matters.

The three key questions every investor faces are:

- Should I contribute to a Roth (post-tax) or Traditional (pre-tax) account?

- Should I max out my 401(k) or other retirement plans?

- How should I allocate assets across my taxable and non-taxable accounts?

Let’s break these down step-by-step.

Roth vs. Traditional – What’s the Difference?

Nick Maggiulli simplifies this debate beautifully in Just Keep Buying Book:

1. Traditional 401(k): Pay Taxes Later

Suppose Annie earns $100. She contributes it directly into her Traditional 401(k) without paying income tax today.

After 30 years, that $100 grows 3x to $300.

When she withdraws it in retirement, she pays 30% tax, leaving her with $210 after taxes.

2. Roth 401(k): Pay Taxes Now, Withdraw Tax-Free Later

Now take Amy, who earns the same $100 but pays her 30% tax today – investing only $70 into her Roth 401(k).

Over 30 years, her investment also grows 3x to $210 – but now it’s completely tax-free when she withdraws it.

So in both cases, Annie and Amy end up with the same $210 in retirement – assuming the tax rate stays constant.

When Roth Might Be Better?

The difference appears if future tax rates rise.

If you expect higher taxes in the future, paying tax now (via a Roth account) is smarter.

Another often-missed detail:

When you “max out” a Roth 401(k), you’re actually putting more real dollars into a tax-sheltered account than with a Traditional 401(k).

Example:

If both Annie and Amy each contribute the maximum limit of $19,500 in 2020 –

- Annie (Traditional) will still owe taxes later. Assuming a 30% tax rate, her $58,500 after growth turns into only $40,950 after retirement taxes.

- Amy (Roth) will keep the full $58,500, completely tax-free.

Bottom line:

Bottom line:

If you think your retirement tax rate will be higher than today, go with Roth.

If you expect it to be lower, a Traditional plan might be better.

Asset Allocation – Where to Keep What

Now comes the confusing part: How to organize your assets across taxable and non-taxable accounts.

There are two types of investment accounts:

- Tax-advantaged accounts – like 401(k)s, IRAs, or Roth IRAs

- Taxable accounts – like regular brokerage accounts

So, where should you keep different types of assets?

Common Confusion: Mixing Assets Across Accounts

Many investors think they should separate assets – for example:

- Stocks in retirement accounts

- Bonds or cash in brokerage accounts

But Nick Maggiulli explains in Just Keep Buying that this approach can cause big problems when it’s time to rebalance.

Example:

Suppose you keep all your stocks in a 401(k) and all your bonds in a brokerage account.

If the stock market crashes and you want to rebalance (buy more stocks while they’re cheap), you can’t transfer cash from your brokerage to your 401(k). Your hands are tied.

That’s why Nick does the same asset allocation across all accounts – a method called “proportional allocation.”

Proportional Allocation Explained

Nick keeps his 401(k), IRA, and brokerage accounts all holding similar types of investments in similar ratios.

For example:

Account Type | Stocks | Bonds |

401(k) | 70% | 30% |

IRA | 70% | 30% |

Brokerage | 70% | 30% |

This balanced approach has three big benefits:

- You can rebalance easily

- You stay diversified across account types.

- You don’t create tax headaches by moving or selling assets.

In short, proportional allocation = simplicity + flexibility + lower tax stress.

Keep It Simple – and Just Keep Buying

Nick Maggiulli’s message is clear throughout Just Keep Buying:

“Complexity kills performance. Simplicity builds wealth.”

So, instead of obsessing over perfect tax hacks or tiny allocation differences – focus on buying consistently and staying invested.

Even the best tax strategy can’t beat the long-term power of regular investing.

Keep your system simple.

Automate your contributions.

And Just Keep Buying – in every account you have.

Just Keep Buying Key Takeaways from Chapter 19

- Roth vs. Traditional: Both can give similar results – but Roth wins if future taxes are higher.

- Maxing Out Accounts: Roth 401(k) gives you more post-tax money in the long run.

- Asset Allocation: Use proportional allocation – keep similar assets across all accounts.

- Avoid Over-Optimization: Rebalancing across accounts gets harder when you separate assets.

- Simplicity Wins: The easiest investment plan is usually the most effective – Just Keep Buying.

Chapter 20: The Illusion of Feeling Rich

(Inspired by “Just Keep Buying” by Nick Maggiulli)

Money Changes, But So Do People

In Just Keep Buying, author Nick Maggiulli reminds us that wealth is not just about numbers – it’s about how we feel about those numbers. You can have millions in the bank and still not feel rich.

Nick begins this chapter with the tragic story of Jack Whittaker, a man who won $314 million in a lottery despite already having a net worth of $17 million.

Instead of becoming happier or fulfilled, Jack’s life spiraled downward – gambling, reckless behavior, and family tragedy followed. His story is a painful reminder that money magnifies who we already are rather than changing us for the better.

The takeaway?

Having money doesn’t always mean feeling rich. Emotional stability and self-control matter far more than the size of your bank account.

“I’m Not Rich – They Are”

Nick Maggiulli shares his own personal moment of realization. Between 2002 to 2007, he felt financially successful – earning well, saving consistently, and building a decent portfolio.

But something changed.

When he compared himself to others doing better – friends driving nicer cars, owning bigger homes, or vacationing more – he suddenly felt poor.

That’s the curse of social comparison – the never-ending race where someone is always ahead.

Even in your best financial phase, if you keep comparing, you’ll always find someone “richer.” It’s like running on a treadmill – you move, but you never really arrive.

Why Even Billionaires Don’t Feel Rich?

You might wonder: “If I had a billion dollars, I’d definitely feel rich!”

But surprisingly, many billionaires don’t.

According to research published in The Review of Economics and Statistics, even the top-earning households often underestimate how well-off they are. Why? Because their reference point isn’t the average person – it’s their peers.

Economist Matthew Jackson explains this through the Friendship Paradox:

“The most popular people appear in many other people’s friendship lists, while those with fewer friends appear on fewer lists.”

In wealth terms – you always “see” the rich people more. They are overrepresented in your awareness because wealth gets visibility: media stories, luxury lifestyles, social media highlights.

So even if you are doing well, your brain tricks you into thinking you’re not – because you keep comparing upward.

Perspective Check: You’re Richer Than You Think

Here’s some perspective Nick gives that can completely shift how you see your finances:

- If your net worth exceeds $4,210, you are wealthier than half of the world.

- If your net worth is above $93,170, you’re already in the top 10% globally.

Let that sink in.

If you live in a developed country, can save, invest, and still have disposable income, you’re already in a position that billions of people would dream of.

The Real Lesson from “Just Keep Buying”

From the entire Just Keep Buying Book, Nick Maggiulli constantly emphasizes one truth:

“Wealth isn’t built by chasing the next big thing – it’s built by consistently doing the right things.”

If you focus on steady investing, long-term growth, and emotional control, you’ll eventually achieve financial freedom – whether you “feel rich” or not.

The secret?

Stop comparing. Start compounding.

Just keep buying.

Example for Better Understanding

Let’s take two friends, Rahul and Aman.

- Rahul earns ₹1 lakh/month and saves ₹30,000 consistently.

- Aman earns ₹5 lakh/month but spends ₹4.9 lakh.

Five years later, Rahul has built ₹18 lakh in investments, while Aman has almost nothing saved.

Guess who feels rich?

Aman, because he shows it.

Guess who is actually rich?

Rahul, because he owns it.

Wealth is quiet. Status is loud.

Just Keeping Buying Key Takeaways from Chapter 20

- Money doesn’t fix emotions – it amplifies them.

- Comparison kills contentment – you’ll always find someone richer.

- Even the wealthy don’t feel rich because they compare with wealthier peers.

- Your real wealth is measured in time, freedom, and peace of mind – not just in rupees or dollars.

- If you can save and invest regularly, you’re already ahead of most of the world.

- Just Keep Buying – focus on your journey, not someone else’s lifestyle.

Chapter 21: Time – The Real Wealth You Own

(Inspired by “Just Keep Buying” by Nick Maggiulli)

Money Can Buy Almost Everything… Except Time

In Just Keep Buying, author Nick Maggiulli delivers one of the most profound messages of the entire book – the most important asset you’ll ever own isn’t money, property, or stocks.

It’s time.

Imagine you’re Warren Buffett at 87 years old – a billionaire, free to buy anything, travel anywhere, and live however you want.

Would you trade your 87-year-old self for your 25-year-old self again, even if it meant losing your billions?

Most people – including Buffett – would say yes.

That’s because time has compounding value, just like money. You can lose money and earn it back. But you can never buy back time once it’s gone.

The Mountain Man Who Moved a Mountain

Back in the 1960s, in a small Indian village called Gehlaur, people had to walk over 50 kilometers around a mountain ridge just to reach the nearest hospital or market.

One day, a villager named Dashrath Manjhi lost his wife because medical help couldn’t reach them in time. Broken-hearted but determined, he made a promise to himself – to carve a road through the mountain so no one would ever suffer the same fate again.

With nothing but a hammer and chisel, Dashrath Manjhi worked every day for 22 years – cutting a 360-foot-long path through solid rock.

He didn’t have money, fame, or technology. What he did have was time, patience, and persistence – the three things more powerful than any investment strategy in the world.

His story reminds us that your time is the true currency of life. How you spend it defines your legacy, not how much you earn.

We Start as Growth Stocks, and End as Value Stocks

Nick Maggiulli beautifully compares human life to investing strategies.

When we’re young, we are like growth stocks – full of potential, energy, and risk-taking ability. We can experiment, fail, and bounce back stronger.

As we age, we slowly become value stocks – stable, cautious, and focused on preservation instead of rapid expansion.

This natural transition is not something to fear. It’s a reminder that every phase of life has its own form of wealth:

- In your 20s → You have time and energy.

- In your 40s → You have skills and experience.

- In your 60s → You have wisdom and stability.

Understanding which “asset class” you are in helps you use your time more wisely.

The Real ROI: Return on Life

We often calculate ROI – Return on Investment – for money.

But very few calculate ROL – Return on Life.

You can earn a high salary, own a luxury home, and still feel poor if you’re trading all your time for money.

On the other hand, someone earning less but spending time on things they love – family, travel, creativity – may feel truly wealthy.

Just like financial assets, time must be allocated intentionally. The difference is – once spent, it never comes back.

So the best way to live the “Just Keep Buying” philosophy is not only to keep buying investments but to keep buying time – by simplifying your life, automating your savings, and creating freedom for what truly matters.

Example for Clarity

Let’s say two friends, Meera and Rohan, both earn ₹1 lakh per month.

- Meera works 16 hours daily, saving 40% of her income but never taking breaks.

- Rohan works 8 hours, saves 25%, but spends time learning new skills, exercising, and volunteering.

Ten years later, Meera may have more money, but Rohan has more balance, health, and freedom.

Rohan’s wealth compounds not just financially – but emotionally and mentally.

That’s what Nick Maggiulli calls true wealth – when your money serves your time, not the other way around.

Just Keep Buying Key Takeaways from Chapter 21

- Time > Money – You can earn money back, but never time.

- Your most valuable asset isn’t in your portfolio – it’s in your calendar.

- Every phase of life has value – youth gives growth, age gives stability.

- Stop trading all your hours for extra income – trade some money for meaning.

- Plan your life like an investment – with time as your main compounding factor.

- Just Keep Buying – not just assets, but more time freedom with every decision.

Conclusion – Keep Building, Keep Growing

At the end of Just Keep Buying by Nick Maggiulli, one simple truth stands tall – wealth isn’t built overnight, and it’s not only about money. It’s about habits, patience, and smart choices made consistently over time.

Whether it’s learning to invest without fear, managing debt wisely, or understanding that time is your most powerful asset – every chapter teaches us to take small steps toward a secure and meaningful life.

We can’t control the market, but we can control our actions. We can’t predict the future, but we can prepare for it. The secret lies in one simple principle – Just Keep Buying – buying knowledge, discipline, and time for yourself.

Remember, the goal isn’t to get rich fast. The goal is to stay consistent and grow stronger year after year – financially, mentally, and emotionally.