Earning More Won’t Fix Your Finances. This Will.

For years, I believed the solution was simple – earn more, and everything else would fall into place.

So I worked harder. Took on extra hours. Switched jobs for a better salary. And every time the increment arrived, something predictable happened – lifestyle upgraded, priorities shifted, comfort increased. But at the end of the month, the same tight feeling was still there. Just at a higher number.

The salary grew. The anxiety didn’t leave.

It took me longer than I’d like to admit to realise the real problem was never the income. It was the absence of a system. Money without direction disappears – whether you earn ₹30,000 or ₹3,00,000 a month.

Ramit Sethi addresses this directly in I Will Teach You to Be Rich – the solution isn’t working harder or earning more. It’s building a simple, automated money management system that tells every rupee exactly where to go before you can think about spending it.

Here is that system – broken into 3 clear buckets that every working professional can set up this weekend.

Why Most Professionals Never Get Ahead Financially?

Most of us believe we’re handling money the right way – until something forces us to look honestly at the pattern.

For years, my own approach was simple and felt completely logical:

Earn → Spend → Save whatever is left → Repeat

The problem? There was rarely anything left. And even when there was, it quietly disappeared before the next salary arrived.

This is the default financial pattern for most working professionals – and it keeps them stuck regardless of how much their salary grows.

The standard advice doesn’t help either. Track every expense. Cut your spending. Show more discipline. So you try – and it works for about two weeks. Then life happens, motivation fades, and the whole system collapses.

Here’s why willpower-based budgeting always fails eventually: our brains are simply not wired for constant delayed gratification. Restricting yourself every single day requires enormous mental energy – and that energy runs out.

Ramit Sethi’s central argument in I Will Teach You to Be Rich cuts straight to the real issue – the problem was never your discipline or your financial knowledge. The problem is the complete absence of structure and automation.

The 3 bucket money management system solves this by replacing willpower with a simple automated structure. You make the decisions once during setup – then the system runs every month on its own, silently, without stress, without reminders, without relying on your motivation.

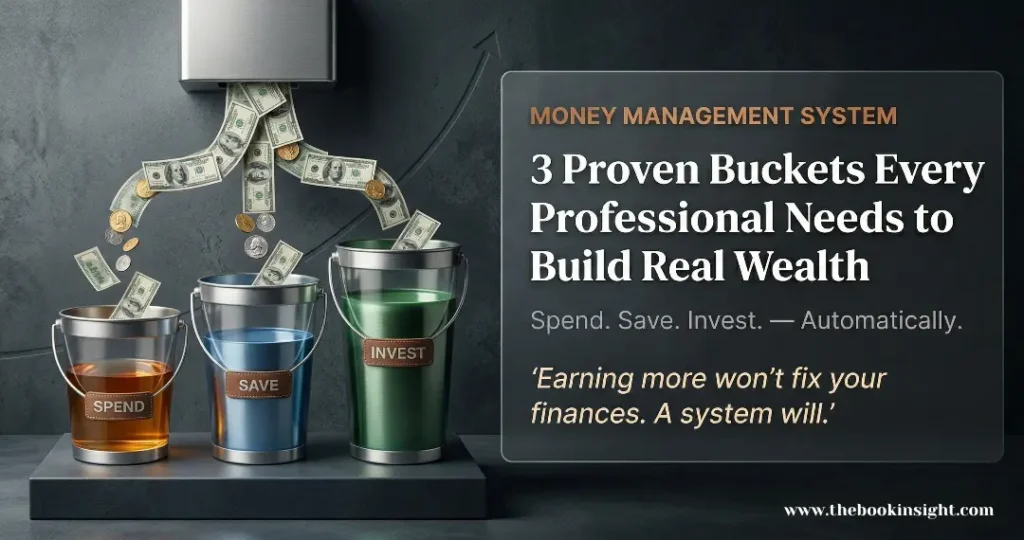

What Is the 3 Bucket Money System?

Before we go into each bucket in detail, here is the complete picture first – because understanding the full map makes every individual step far clearer.

The concept is simple: every rupee you earn gets divided into 3 dedicated buckets the moment your salary arrives. No mid-month confusion. No decision fatigue. No wondering where the money should go.

Here are the 3 buckets at a glance:

- Bucket 1 – Spend: Your monthly fixed costs and lifestyle expenses. Everything you need to live comfortably – rent, bills, groceries, dining, entertainment. This bucket gives you a clear spending boundary so you never overspend without realising it.

- Bucket 2 – Save: Your emergency fund and short-term goals. Life is unpredictable – this bucket exists for the moments you didn’t plan for, and the goals you’re working toward.

- Bucket 3 – Invest: Your long-term wealth engine. Most professionals delay this bucket the longest – usually because of fear, confusion, or simply not knowing where to begin.

The core principle behind the entire system is this: pay yourself first. Savings and investments leave your account automatically on salary day – before lifestyle spending begins, before temptation arrives.

The result? Whatever remains in Bucket 1 is yours to spend completely guilt-free.

Let’s break down each bucket in detail.

The 3 Buckets in Detail

Bucket 1 – The Spend Bucket: Give Yourself Permission to Live

The most misunderstood part of any money management system is this – people assume it means restricting everything and living like a monk. Ramit Sethi completely disagrees. And honestly, so do I.

The real problem is not spending. It is unconscious spending – buying things without a single deliberate thought, and then wondering where the salary disappeared.

Bucket 1 covers everything you spend money on monthly:

- Fixed costs – rent, EMIs, electricity, groceries, transportation, subscriptions

- Guilt-free spending – dining out, entertainment, travel, fitness, whatever genuinely adds joy to your life

Recommended allocation: 50–60% of your take-home income

Ramit’s most practical insight here is surprisingly liberating – identify your 2–3 biggest spending joys and spend on those freely and without guilt. Then cut ruthlessly on everything else that genuinely doesn’t matter to you.

The honest truth is that most professionals overspend not on big things but on small unconscious ones – one extra subscription, one more cigarette packet, one spontaneous dinner that felt harmless. None of these feel significant alone. Together they silently consume 10–15% of your income every month.

The practical setup is simple: list every monthly expense and categorise each one as fixed or lifestyle. If the total crosses 60% of your income, that list will show you exactly where to trim – often it surprises people to see their own spending habits reflected back clearly.

You don’t need to stop spending. You need to spend on the right things – intentionally.

Bucket 2 – The Save Bucket: Build Your Financial Safety Net First

Here is the habit that most working professionals never develop – and quietly regret when life surprises them.

Most people save whatever is left at the end of the month. Ramit Sethi calls this the single biggest financial mistake a professional can make. And the painful reality is – there is rarely anything left. Because spending always expands to fill whatever is available.

Saving must happen first. Automatically. Before lifestyle spending even begins.

Recommended allocation: 10–20% of take-home income

This bucket holds two important things:

- Emergency fund – 3 to 6 months of your living expenses sitting in a separate, easily accessible account. This is your financial floor. Before any investment, before any short-term goal – this comes first. Life is unpredictable, and this fund is what prevents one unexpected event from derailing everything else.

- Short-term goals – house down payment, car, wedding, travel, or any large planned expense. Break the goal into a monthly number and automate it.

A simple example: if you want to take a ₹1 lakh trip in 10 months, that is ₹10,000 per month into this bucket. Clear, simple, automatic – no stress when the trip arrives.

The critical distinction most professionals miss: investments and savings are not the same thing. Investments carry market risk. Savings carry security. Both are essential – but savings come first.

The automation principle makes this effortless – set up an automatic transfer on salary day so the money moves to a separate savings account before you see it, before you spend it, before you even think about it.

Saving is not what you do with what’s left. It’s the first decision you make when money arrives.

Bucket 3 – The Invest Bucket: Make Your Money Work While You Sleep

This is the bucket most professionals delay the longest – and that delay is quietly the most expensive financial mistake they will ever make.

Not because investing is complicated. But because fear, confusion, and the comfortable belief that “I’ll start when I earn more” keeps pushing it further into the future.

This bucket is not about savings accounts or fixed deposits. It is about instruments that grow faster than inflation and compound silently over decades – SIPs in mutual funds, index funds, PPF, NPS, and stocks.

Recommended allocation: 20–30% of take-home income

One important thing most professionals miss when calculating investment returns – always adjust for inflation. A 12% annual return sounds impressive until you subtract 6% inflation. Your real return is closer to 6%.

Use an inflation calculator to see your actual wealth growth, not just the headline number.

The compounding reality is impossible to ignore once you see it clearly:

₹5,000 per month invested at 12% annual return over 20 years = approximately ₹49 lakhs. The same ₹5,000 sitting in a savings account for 20 years barely keeps pace with rising prices.

The three reasons professionals delay this bucket – and all three are costly:

- “I’ll start when I earn more”

- “I’ll start when I understand investing better”

- “I’ll start when the market is right”

Every month of delay is compounding working against you instead of for you.

Ramit’s principle here is clear and practical: start now, start small, automate it completely. A SIP of ₹2,000 started today will build more wealth than a SIP of ₹10,000 you keep planning for next year.

If starting at 20–30% feels overwhelming right now, begin with whatever is realistic – even 5% or 10%. Then increase by just 1% every six months. The habit matters more than the amount in the beginning.

Set up your SIP on the 2nd or 3rd of every month – right after salary arrives, right after the Save bucket moves automatically. Your money management system then runs completely on its own.

The best time to start investing was yesterday. The second best time is today – automated, consistent, and forgotten.

How to Set Up Your 3 Bucket System This Weekend?

You now have the complete picture. Here is how to turn it into a working system within 48 hours – no financial expertise required.

Step 1 – Calculate your exact take-home monthly income. Not your CTC. Your actual in-hand salary after all deductions. This is the number your entire system is built around.

Step 2 – Open 2 separate bank accounts if you don’t already have them. One dedicated account for your Save bucket. Your existing primary account becomes your Spend bucket. Keep them completely separate – out of sight genuinely means out of mind.

Step 3 – Set up automatic transfers on salary day. Save bucket moves first. Invest SIP moves second. Both happen automatically within 24 hours of salary credit – before your spending begins, before your brain starts making decisions.

Step 4 – Whatever remains is yours completely. The amount sitting in your primary account after the automatic transfers is your guilt-free Spend bucket for the entire month. Spend it without stress, without tracking, without guilt.

That is the entire 3 bucket money management system – built once, running forever.

No daily discipline required. No monthly reminders. No stress about managing everything simultaneously. The automation does the one thing willpower never could – it works consistently whether you are motivated or not.

For Ramit Sethi’s complete financial framework, read our full I Will Teach You to Be Rich summary here.

Frequently Asked Questions

Real questions people search about this topic — answered directly.

A general starting point from Ramit Sethi's framework: 50–60% into Spend, 10–20% into Save, and 20–30% into Invest. These are not rigid rules – adjust based on your income level, EMI obligations, and current financial stage. The key principle is that Save and Invest buckets move automatically before Spend begins.

Absolutely — in fact, this system works better on a modest salary because it forces intentional allocation from day one. Start with whatever percentages are realistic. Even saving 5% and investing 5% is infinitely better than saving nothing. Increase the percentages by 1–2% every time your income grows.

The Save bucket is for security and short-term goals – money that must be accessible and safe. The Invest bucket is for long-term wealth – money that can tolerate market fluctuation because it won't be needed for years. Both are essential. One protects you today. The other builds your future.

High-interest debt like credit card debt should be prioritised aggressively – treat debt repayment as a fourth bucket temporarily. For low-interest debt like home loans or education loans, you can run the 3 bucket system alongside regular EMI payments, which typically sit inside the Spend bucket as a fixed cost.

Traditional budgeting tracks every expense and requires constant monitoring. The 3 bucket money management system is built on automation – you make the decisions once during setup, then the system runs itself every month. Less willpower. Less tracking. More consistency.

Conclusion: One Decision That Changes Your Financial Life

The professionals who build real wealth over time are not necessarily the highest earners in the room. They are simply the ones who decided – at some point – to stop letting money flow wherever it wanted and start directing it with intention.

The gap is never income. It is always the presence or absence of a system.

The 3 bucket money management system does not ask you to be perfect with money. It asks you to make one decision, set it up once, and let automation handle everything else from that day forward.

Before you close this page, sit with one honest question:

“At the end of this month, will your money have gone somewhere intentional – or just somewhere?”

Your answer tells you exactly where to begin.

For the complete framework behind these ideas, read our full I Will Teach You to Be Rich summary here – it will permanently change how you think about money.

If this helped you see your finances differently, share it with someone who needs to hear it today.